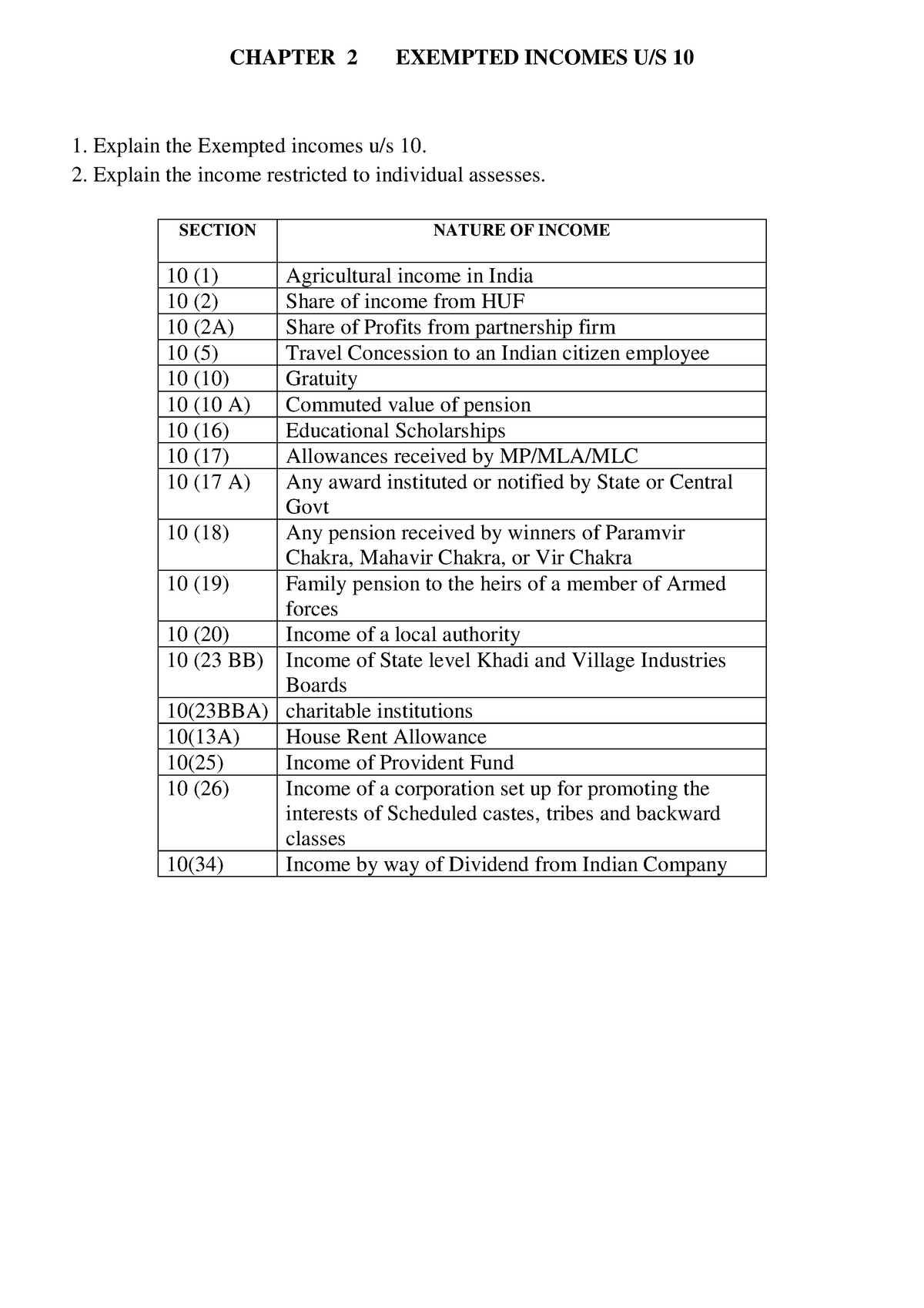

People are not able to buy property when you look at the dollars. Needless to say, no financial lets you borrow money free of charge. You’ll be billed interest, with a performance influenced by situations that are included with the present day desire speed ecosystem, the lending company as well as your personal credit score .

Mortgage loans was advanced products which use a method entitled amortization to help you allow borrowers to expend a typical rate across the entirety off the loan, that’s basically between 15 and thirty years . But mortgage amortization is actually a comparatively obscure build to many people, together with really home loan people.

Focusing on how it functions ahead of time selecting a mortgage, consider makes it possible to get a good idea of exactly where your money is certainly going and just why.

How come home loan amortization work?

Understanding how amortization works can make you a conscious consumer regarding mortgage loans and provide all the information you need to thought significantly about your money total.

Financial principles

It helps so you can basic discover just what home financing is actually and you may the way it operates. Home financing try a loan out of a financial used to buy a home, that finance generally end up in one of two groups: fixed-rates or variable .

A predetermined-speed home loan means your lock in the rate of interest when you purchase your home, and therefore stays the pace towards entirety of mortgage. Incase you don’t refinance otherwise offer your residence, you can improve exact same payment per month towards the totality away from your financial.

A varying-rates home loan (ARM), on the other hand, has an interest price one to changes into the an appartment schedule. An arm generally starts with a predetermined speed to have a flat period, that’s followed by possible speed alterations on a flat agenda.

You’ll generally see a supply loan with a few number. The original informs you the fresh place speed several months, as well as the second the newest agenda to own price alter. Including, an excellent 5/1 Arm have a-flat speed age of five years, and then the speed would be adjusted one time per year.

Amortization basics

“Amortization allows for new borrower getting a fixed fee over the period period,” states Bill Banfield, government vice-president from capital places in the Rocket Financial. “Just what it cannot create is actually possess the same number of principal and interest.”

With an enthusiastic amortized mortgage plan, the loan money go mostly toward notice towards the earliest several years of your loan, leaving the primary mainly unaltered. Over time, more of the fee monthly goes toward the principal, and this continues till the loan is totally paid back.

The level of notice and you can principal you have to pay every month is calculated playing with an intricate formula. This is how it works:

There are even an abundance of calculators available online that may allow you to find out how your home loan amortization agenda works.

Remember that their payment commonly still differ for people who possess a supply, since the interest rate can change through the years.

Exactly how early payments can help

If you’d like to repay your financial early and you may rescue on the focus, you could make early repayments on your dominant. One way to accomplish that will be to setup a schedule you to Banfield described as “an old-designed solution” – and come up with mortgage repayments all the two weeks.

“The good most important factor of doing it online payday loans Oklahoma biweekly, it’s actually 26 money per year. You’ve got the ability to pay even more dominant,” Banfield states.

Settling extra dominating using your loan ensures that you can actually pay off the loan before your 31-season mortgage title is more than, which there are less overall regarding loan racking upwards interest.

This one is particularly attractive when you have a high financial interest rate, including the of those offered immediately . For many who purchased your property while in the a lower-speed several months, you may be better off putting that money with the sector or in a leading-produce family savings .

The conclusion

Financial amortization was something regularly make sure borrowers has actually consistent money along the life of its financing, just in case you utilize a fixed-speed home loan. With Palms, new percentage tend to fluctuate according to rate customizations. It is a relatively difficult procedure, but well worth skills if you’re planning to invest in a house.